@altgate

Startups, Venture Capital & Everything In BetweenRecent Posts

-

How Much to Build That Mobile App?

At ExtensionEngine we recently launched an online budget estimating tool for mobile apps and I..

-

We Need an “NTSB” for Entrepreneurship

Every time an airplane crashes or even has an incident in the US, the NTSB..

-

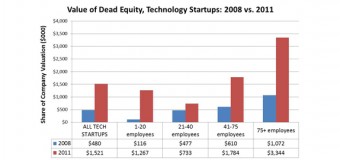

Is Dead Equity Crippling Your Company?

Re-posted from post co-authored with Prof. Noam Wasserman on Inc. —————– Dead equity — equity held..

-

Solving the Dark Data Puzzle

Repost from my work blog. —————- In this era of Big Data where more than..

-

How Does Your Company Stack Up?

Compensation at startups is different than almost any other kind of organization you might join..

-

Fear vs. Greed at Facebook

This is a repost of an article written by Prof. Noam Wasserman and myself. ——————————-..

-

4 Top Myths About Start-up Pay

This is a repost of an article written for Inc.com by Prof. Noam Wasserman and..

-

Are You Ready for the Post-Flash World?

Flash for mobile is dead. Can Flash for desktops be far behind? That is the..

-

iPad in the Enterprise

Yesterday I finally received and read iPad in the Enterprise that I had pre-ordered a..

-

Top 10 Tips For Developing Enterprise Mobile Apps

I wrote this post, the full version of which is over at extensionEngine. Every year..